What is a cost type contract? It’s a type of agreement where the buyer pays the seller for all allowable costs incurred in completing a project, plus a predetermined fee. Unlike fixed-price contracts where the total cost is set upfront, cost-type contracts offer flexibility but shift more risk to the buyer. This approach is particularly useful for projects with uncertain scopes or technological advancements, allowing for adjustments as the work progresses.

Understanding the nuances of cost-type contracts is crucial for both buyers and sellers. Different variations exist, each with its own risk-reward balance. Careful planning, clear communication, and robust monitoring are key to successful cost-type contracts, ensuring a fair outcome for all parties involved. This involves defining allowable costs, establishing payment mechanisms, and agreeing on a fee structure. The following sections delve into the intricacies of these contracts, providing a comprehensive overview for informed decision-making.

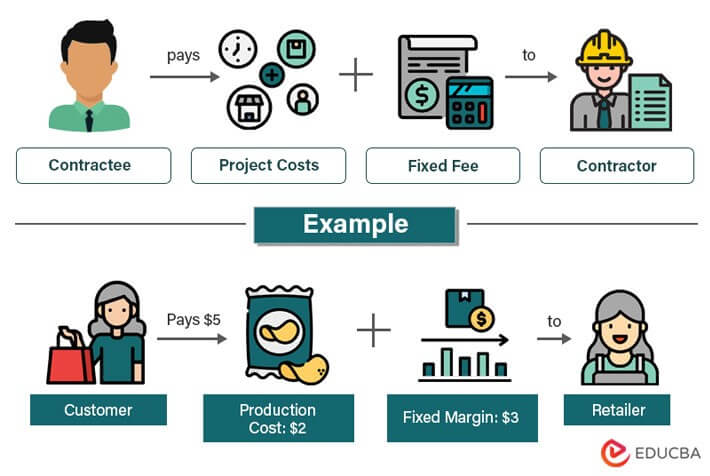

Definition of Cost-Type Contracts

Cost-type contracts represent a fundamental approach to procurement where the buyer reimburses the seller for allowable costs incurred in fulfilling a project, plus a fee, often a fixed percentage or a predetermined amount. This structure differs significantly from fixed-price contracts, placing a greater emphasis on collaboration and transparency between the parties.Cost-type contracts are best suited for projects with high uncertainty, complex technical requirements, or a need for significant flexibility throughout the project lifecycle.

They are commonly employed in situations where the precise scope of work is difficult to define upfront, such as research and development projects or complex construction endeavors.

Fundamental Characteristics of Cost-Type Contracts

Cost-type contracts share several key characteristics. First, the seller’s payment is directly tied to the actual costs incurred in performing the work. Second, the contract explicitly defines allowable costs, setting boundaries on what expenses the buyer will reimburse. Third, a fee structure is incorporated, providing the seller with compensation for its efforts and risk. This fee can be fixed, incentivized (based on performance), or a combination of both.

Finally, detailed record-keeping and cost reporting are essential elements, ensuring transparency and accountability.

A Concise Definition for a Lay Audience

Imagine hiring a contractor to renovate your home. In a cost-type contract, you agree to pay the contractor for all the materials and labor they use, plus a set fee for their services. The total cost isn’t known upfront, but you trust the contractor to manage the project efficiently.

Core Principle Differentiating Cost-Type Contracts

The core principle differentiating cost-type contracts from other contract types, such as fixed-price contracts, lies in the allocation of risk. In cost-type contracts, a significant portion of the cost risk is transferred to the buyer. The seller is reimbursed for allowable costs, irrespective of whether they exceed initial estimates. Conversely, in fixed-price contracts, the seller bears the primary cost risk.

Comparison of Cost-Type and Fixed-Price Contracts

The following table contrasts key features of cost-type and fixed-price contracts:

| Feature | Cost-Type Contract | Fixed-Price Contract |

|---|---|---|

| Risk Allocation | Primarily on the buyer | Primarily on the seller |

| Cost Certainty | Low | High |

| Payment Method | Reimbursement of allowable costs plus fee | Lump sum or milestone payments |

| Suitability | Projects with high uncertainty or evolving requirements | Projects with well-defined scope and predictable costs |

Types of Cost-Type Contracts

Cost-type contracts, unlike fixed-price contracts, reimburse the contractor for allowable costs incurred in performing the work. The level of risk borne by the contractor and the government (or client) varies significantly depending on the specific type of cost-type contract employed. This necessitates a careful consideration of the project’s complexity, uncertainty, and the desired level of control.

Cost-Plus-Fixed-Fee (CPFF) Contracts

CPFF contracts reimburse the contractor for all allowable costs incurred, plus a fixed fee agreed upon in advance. The fixed fee compensates the contractor for its overhead and profit, regardless of the actual costs incurred. This structure provides a degree of cost certainty for the government, as the fee is predetermined. However, the contractor has an incentive to manage costs efficiently, as its profit is not directly tied to the total cost.

Case Study: Imagine a government agency contracting with a firm to develop a new radar system. The specifications are complex, and the development process is likely to involve unforeseen challenges. A CPFF contract would allow for flexibility in addressing these challenges while still providing a predictable cost ceiling for the agency. The fixed fee would cover the contractor’s profit and overhead, regardless of whether the project comes in under or over budget.

Industries:

- Defense and Aerospace

- Research and Development

- Government contracting

Cost-Plus-Incentive-Fee (CPIF) Contracts

CPIF contracts also reimburse allowable costs, but the fee is structured as a variable amount that depends on the contractor’s performance against pre-defined targets. This incentivizes cost efficiency and performance, offering a shared risk and reward between the contractor and the government. Performance targets might include cost, schedule, and technical performance metrics.

Case Study: Consider a construction project for a large hospital. A CPIF contract could be used, with incentives tied to meeting the project’s budget, completion date, and quality standards. If the contractor exceeds the targets, it receives a higher fee; if it falls short, the fee is reduced. This approach encourages the contractor to proactively manage costs and performance.

Industries:

- Construction

- Engineering

- Information Technology

Cost-Plus-Percentage-of-Cost (CPPC) Contracts

CPPC contracts reimburse allowable costs plus a percentage of those costs as a fee. This structure, while straightforward, is generally less favored due to the potential for cost overruns. The contractor’s profit is directly proportional to the total cost, creating an incentive to inflate costs. This type of contract is less common today due to the inherent risk of cost escalation.

Case Study: Historically, CPPC contracts were sometimes used in situations where uncertainty was extremely high, such as early stages of research and development. However, the inherent risk associated with this type of contract has led to its decreased popularity. For instance, a pharmaceutical company might have used this in early clinical trials, but the inherent cost risk would be significant.

Industries:

- Historically used in some niche areas of R&D, but now largely replaced by other contract types.

Cost-Type Contract Components: What Is A Cost Type Contract

Cost-type contracts, unlike fixed-price contracts, involve a reimbursement mechanism where the contractor is compensated for allowable costs incurred during project execution, plus a fee. Understanding the components of these contracts is crucial for both contractors and clients to manage risk and ensure fair compensation. The clarity and precision with which these components are defined directly impact the success and financial stability of the project.

The core elements of a cost-type contract include the definition of allowable costs, the reimbursement methodology, and the fee structure. Misunderstandings or ambiguities in any of these areas can lead to significant disputes and financial losses. Therefore, a well-defined contract, meticulously outlining each component, is paramount.

Allowable Costs

Allowable costs represent the expenses the client agrees to reimburse the contractor. This definition is contractually specified and typically includes direct and indirect costs. Direct costs are directly attributable to the specific project, such as labor, materials, and equipment. Indirect costs, also known as overhead costs, are less directly related but necessary for project completion, such as administrative expenses and rent.

The contract must explicitly list what constitutes allowable costs, and what does not, to prevent disputes. For example, a contract might exclude certain types of entertainment expenses or specific types of travel. The more detailed the definition, the less room for disagreement.

Reimbursement Mechanisms

Several methods exist for reimbursing the contractor for allowable costs. The most common include cost-plus-fixed-fee (CPFF), cost-plus-incentive-fee (CPIF), and cost-plus-award-fee (CPAF). Each method presents a different risk-sharing profile between the client and the contractor. For instance, under a CPFF contract, the contractor receives reimbursement for all allowable costs plus a predetermined fixed fee, regardless of the final project cost.

This minimizes the contractor’s financial risk but potentially increases the client’s. In contrast, a CPIF contract introduces incentives for cost control, aligning the interests of both parties.

Fee Structures, What is a cost type contract

The fee structure defines how the contractor is compensated beyond the reimbursement of allowable costs. Common fee structures include fixed fees, incentive fees, and award fees. A fixed fee is a predetermined amount paid to the contractor irrespective of the actual costs incurred. Incentive fees are contingent upon achieving specific performance targets, rewarding efficiency and cost control.

Award fees are based on subjective evaluations of the contractor’s performance, providing flexibility but also introducing potential subjectivity into the compensation process. The choice of fee structure depends on the project’s complexity, risk profile, and the desired level of contractor motivation.

Cost Calculation Under a Cost-Plus-Fixed-Fee Contract

Calculating costs under a CPFF contract involves a straightforward process. First, all allowable costs are meticulously documented and categorized. This involves gathering receipts, invoices, and timesheets, ensuring all expenses align with the contract’s definition of allowable costs. Second, these documented costs are then summarized and verified for accuracy. Finally, the pre-agreed fixed fee is added to the total allowable costs to arrive at the final contract price.

Total Contract Price = Total Allowable Costs + Fixed Fee

For example, if a project incurs $1 million in allowable costs and has a fixed fee of $100,000, the total contract price would be $1.1 million. The importance of accurate cost tracking and adherence to the contract’s definition of allowable costs cannot be overstated. Any deviation can lead to disputes and renegotiations. Transparency and detailed record-keeping are crucial for successful cost management within a CPFF framework.

Risk and Reward Allocation in Cost-Type Contracts

Cost-type contracts, while offering flexibility, present a unique allocation of risk and reward between the buyer (typically the government or a large corporation) and the seller (the contractor). The degree of risk and reward borne by each party varies significantly depending on the specific type of cost-type contract employed. Understanding this dynamic is crucial for effective contract negotiation and management.The fundamental principle is that greater cost risk is assumed by the buyer in exchange for potentially greater cost savings and innovative solutions from the seller.

Conversely, greater cost certainty is achieved by the buyer when they assume less risk, but this often comes at the expense of potentially higher costs.

Risk and Reward Allocation in Different Cost-Type Contracts

Cost-type contracts distribute risk and reward differently based on their structure. In a cost-plus-fixed-fee (CPFF) contract, the buyer assumes the majority of the cost risk, as the seller is reimbursed for all allowable costs up to a pre-agreed ceiling, plus a fixed fee regardless of the actual cost incurred. The seller’s reward is limited to the fixed fee, incentivizing them to complete the project efficiently but not necessarily to control costs aggressively.

In contrast, a cost-plus-incentive-fee (CPIF) contract shifts a portion of the cost risk to the seller by introducing a shared savings or loss mechanism. The seller earns a larger fee if they complete the project under budget and may incur a penalty or reduced fee if costs exceed targets. This arrangement encourages cost control and efficiency. Finally, a cost-plus-award-fee (CPAF) contract places even more emphasis on performance and incentivizes the seller to go above and beyond the minimum requirements.

The award fee is subjective and based on the buyer’s assessment of the seller’s performance, fostering a strong emphasis on quality and innovation.

Comparison of CPFF and CPIF Contract Risk Profiles

The CPFF contract presents a higher risk profile for the buyer compared to the CPIF contract. The buyer in a CPFF arrangement bears the brunt of cost overruns, as the seller’s fee remains fixed regardless of actual costs. The seller, conversely, faces a lower risk profile, enjoying a guaranteed profit regardless of project cost. This can potentially lead to less emphasis on cost control by the seller.

The CPIF contract, however, mitigates this risk by incorporating incentives. The shared savings or loss mechanism incentivizes the seller to actively manage costs, thereby reducing the buyer’s exposure to cost overruns. While the buyer still bears some risk, it is significantly reduced compared to the CPFF model. The seller’s reward is directly tied to cost performance, leading to a more balanced risk-reward distribution.

This shared risk incentivizes collaboration and proactive cost management between buyer and seller.

Incentive Mechanisms in Cost-Plus-Incentive-Fee Contracts

CPIF contracts employ several mechanisms to incentivize cost control. These mechanisms are typically defined in the contract’s incentive fee structure, which Artikels the target cost, the ceiling price (the maximum amount the buyer will pay), and the sharing ratio for cost savings or overruns. For instance, a contract might stipulate a 50/50 sharing ratio, meaning that cost savings are split evenly between the buyer and the seller, while cost overruns are also shared proportionally.

This structure creates a direct link between the seller’s cost management and their profitability. Further incentives might include performance-based milestones or bonuses tied to achieving specific cost targets or exceeding performance expectations. These mechanisms encourage collaboration and shared responsibility for cost control, aligning the interests of both parties and fostering a more efficient and effective project execution.

Effective implementation necessitates clearly defined metrics, transparent cost tracking, and a robust communication channel between the buyer and seller.

Contract Administration and Monitoring

Effective administration and monitoring are crucial for successful cost-type contracts. These processes ensure the project stays on track, costs remain within budget, and the relationship between the contracting parties remains productive. Without rigorous oversight, cost overruns and disputes are significantly more likely.

Administering and monitoring cost-type contracts involves a multifaceted approach encompassing regular communication, meticulous record-keeping, and proactive risk management. This requires a clearly defined set of procedures, agreed-upon metrics, and a dedicated team responsible for tracking progress and managing potential issues. The level of oversight will naturally vary depending on the contract’s complexity and value.

Procedures for Administering and Monitoring Cost-Type Contracts

Effective administration involves establishing clear communication channels, implementing a robust system for tracking costs and deliverables, and conducting regular performance reviews. This includes establishing a formal process for submitting and approving cost reports, performing regular site visits (where applicable), and maintaining open communication between the contractor and the contracting authority. Discrepancies should be addressed promptly, and changes to the scope of work should follow established change management procedures, documented meticulously and approved by both parties.

The use of project management software can significantly enhance the efficiency of these processes.

Common Challenges in Administering Cost-Type Contracts and Mitigation Strategies

Several challenges frequently arise in administering cost-type contracts. One common issue is the potential for cost overruns, driven by unforeseen circumstances or inefficient contractor practices. Mitigation strategies include implementing robust cost control mechanisms, utilizing independent cost estimates, and establishing clear performance incentives that align the contractor’s interests with cost efficiency. Another challenge involves disputes over allowable costs. Clear contract language defining allowable and unallowable costs, coupled with regular audits and transparent cost reporting, can significantly reduce such disputes.

Finally, communication breakdowns between the contracting parties can hinder progress and lead to misunderstandings. Regular meetings, formal communication protocols, and proactive conflict resolution mechanisms can help mitigate this risk. For example, a clearly defined escalation path for resolving disputes, detailed in the contract, helps prevent minor issues from escalating into major conflicts. Consider a scenario where a contractor requests payment for an unanticipated expense.

If the contract clearly Artikels the process for approving such requests and the types of expenses that are reimbursable, the dispute is much less likely.

Checklist for Effective Contract Administration

A comprehensive checklist helps ensure all critical aspects of contract administration are addressed consistently. This checklist provides a framework for effective oversight, ensuring compliance with contractual obligations and minimizing potential risks.

| Category | Task | Frequency | Responsible Party |

|---|---|---|---|

| Cost Monitoring | Review contractor’s cost reports for accuracy and completeness | Monthly | Contract Administrator |

| Performance Monitoring | Track progress against milestones and deliverables | Weekly/Monthly | Project Manager |

| Communication | Hold regular meetings with the contractor | Bi-weekly | Contract Administrator & Project Manager |

| Risk Management | Identify and assess potential risks | Quarterly | Risk Management Team |

| Compliance | Ensure compliance with all applicable regulations | Ongoing | Legal Department |

| Documentation | Maintain complete and accurate records | Ongoing | Contract Administrator |

| Change Management | Manage and document all changes to the contract | As needed | Contract Administrator & Project Manager |

| Payment Processing | Process payments according to the contract terms | Monthly | Finance Department |

Ultimately, choosing the right contract type hinges on the project’s nature, the level of risk tolerance, and the relationship between the buyer and seller. Cost-type contracts, while offering flexibility, require careful management and clear communication to mitigate potential cost overruns. By understanding the various types, components, and risk allocation mechanisms, both parties can enter into a cost-type contract with confidence, fostering a collaborative and successful project outcome.

FAQ Compilation

What are some common reasons for disputes in cost-type contracts?

Disputes often arise from unclear definitions of allowable costs, inadequate cost tracking, and disagreements over the interpretation of contract terms. Poor communication and a lack of transparency can also exacerbate conflicts.

How can a buyer protect themselves in a cost-type contract?

Buyers can mitigate risk by carefully defining allowable costs, establishing robust cost control mechanisms, regular monitoring, and employing independent cost audits.

What are the advantages of using a cost-plus-incentive-fee contract?

This type incentivizes the seller to control costs, as their fee is tied to achieving cost targets. It promotes collaboration and shared risk, leading to potentially lower overall costs and better project outcomes.

When is a cost-type contract not suitable?

Cost-type contracts are less suitable for projects with well-defined scopes and predictable costs, where a fixed-price contract offers greater cost certainty and risk allocation.